In Hong Kong, corporate income tax (profit tax) is levied under the Inland Revenue Ordinance (Cap. 112). When a company incurs losses during a tax year, these losses may be treated and declared under specific provisions. This article provides a detailed explanation of how corporate losses are treated and the relevant provisions of the Inland Revenue Ordinance.

Loss carrying forward

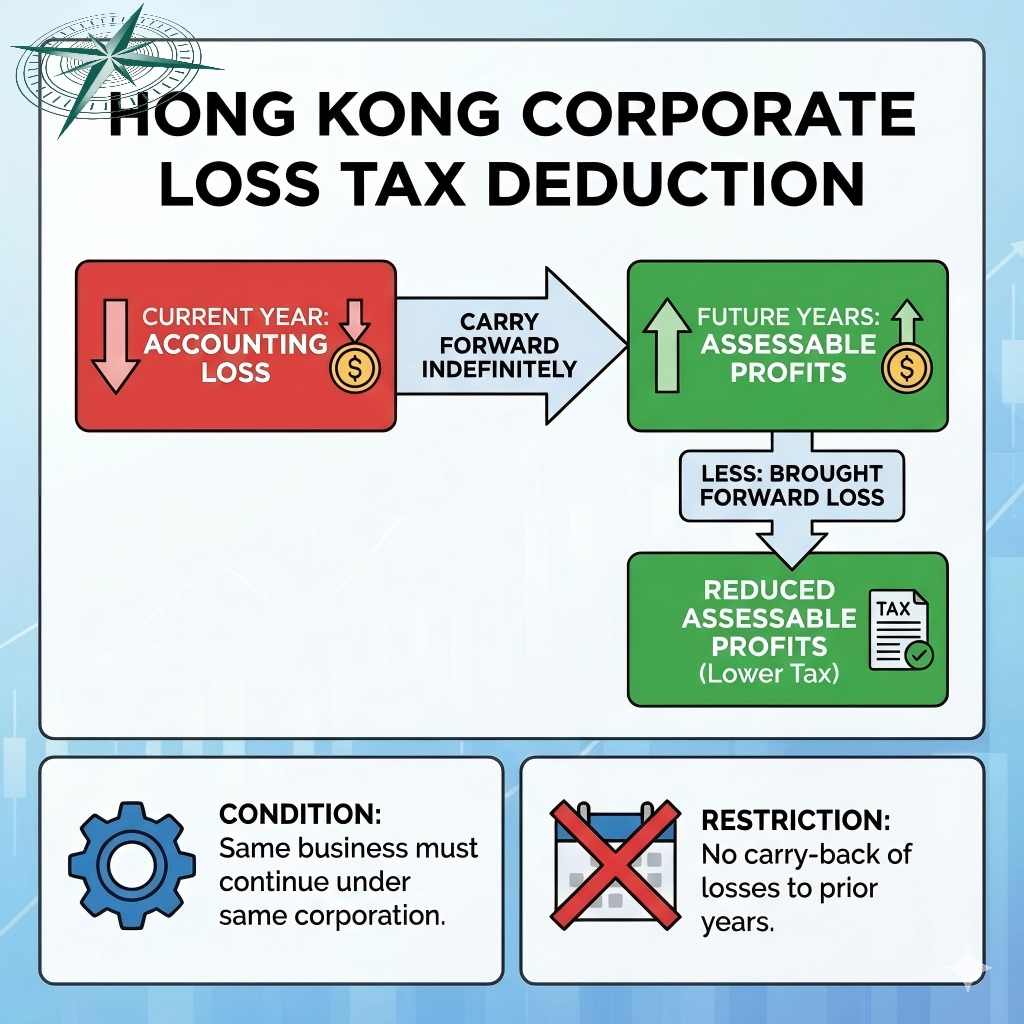

Under Section 19C of the Tax Regulations, losses incurred by a company during a tax year may be carried forward to offset future taxable profits. This allows businesses to utilize prior losses to reduce future tax liabilities when profits are realized.

Tax Ordinance – Article 19C

Under Article 19C of the Tax Ordinance, the specific provisions are as follows:

Article 19C: Handling of Losses (After April 1, 1975)

- Personal trade, professional or business activities:

- If an individual incurs a loss in any trade, profession, or business during a tax year and neither the individual nor their spouse (if the spouse is not separated from them) opts for individual assessment under Section 41, the loss amount shall be carried forward to the subsequent tax year and deducted from the taxable profit in that trade, profession, or business.

2.Losses in a partnership:

- If an individual incurs a loss in the partnership they participate in during any tax year, and the individual or their spouse (if the spouse is not separated from them) does not opt for individual assessment under Section 41, the loss share shall be carried forward to the subsequent tax year and offset against their taxable profit share in the partnership.

3.Loss treatment under personal assessment:

- If an individual incurs a loss or a loss share in a partnership during any tax year and opts for individual assessment under Part 7, the loss or loss share shall be treated under that part.

4.Corporate or non-personal loss:

- If a company or non-personal entity incurs losses in its trade, professional, or business operations during any tax year, the amount of such losses shall be deducted from the company’s taxable profit and carried forward to subsequent tax years to offset its taxable profit.

5.Corporate or non-personal losses in partnerships:

- If any partner in a partnership is a corporation or a non-personal entity and incurs a loss during any tax year, the corporation’s loss share shall be deducted from its taxable profit and carried forward to the subsequent tax year.

6.Loss calculation and transfer rules:

- The amount of loss deduction, once claimed in any tax year, cannot be claimed again in subsequent years.

- Any loss carried forward to a subsequent fiscal year cannot be deducted again.

- The total amount of deductions shall not exceed the loss amount.

- The loss should be attributed to the income from activities in Hong Kong.

- The loss of the trust beneficiary is only deductible against the taxable profit of the trust.

Is there a time limit for transferring losses?

The Hong Kong Tax Ordinance does not impose a time limit on the carry-forward of losses. This allows companies to carry forward losses indefinitely until they fully offset future taxable profits.

Statement of loss

When filing tax returns, companies must document their losses in detail, including the exact amount, the year they occurred, and their sources. These records help the tax authorities verify the legality and accuracy of the losses during audits.

Limitation of loss offset

Although Hong Kong permits the carrying forward of losses, the offsetting of losses may be restricted in certain circumstances. For example:

- Business Transfer: Under Section 61B of the Tax Ordinance, the carry-forward of losses may be restricted if there is a significant change in the company’s business or equity.

Tax planning advice

Companies should conduct regular tax planning to maximize the benefits of loss carryforward policies. Proper financial and tax planning can help reduce future tax burdens and improve financial health.

Summary

Hong Kong’s tax regulations provide businesses with flexible loss carryforward policies, allowing companies to offset future taxable profits by carrying forward losses to subsequent years. Companies should fully utilize this policy while maintaining detailed records and ensuring compliance with all loss-related requirements to pass tax audits smoothly. Through effective tax planning, businesses can reduce their tax burden, enhance operational efficiency, and strengthen their competitive edge.