How should rental properties be taxed? Many prospective property investors have questions about property tax calculations. To accurately determine investment property returns, it’s essential not only to understand stamp duty for property purchases but also to master the’ Property Tax Calculation ‘guide. This article will explain how property tax is calculated under different circumstances. If you’re looking to save on taxes, keep reading.

Income from lease of property

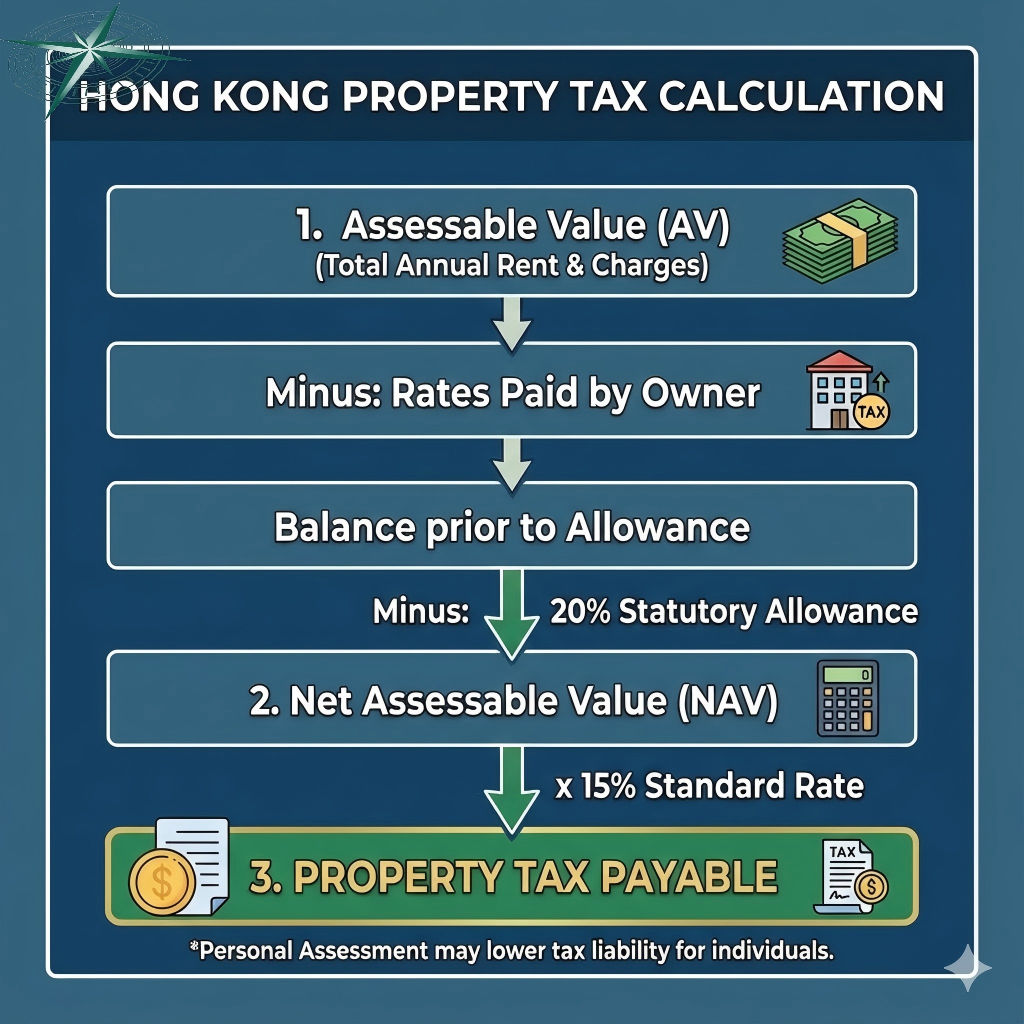

Property Tax Calculation is based on the assessed value of the property in the tax year, calculated at the standard tax rate. The tax year for property tax runs from April 1 to March 31 of the following year.

Property tax formula

The taxable net value for property leasing is calculated as follows:

| A | rent income |

| B | unrecoverable rent |

| C | Appraised Taxable Value (A-B) |

| D | rates paid by owners |

| E | (C-D) |

| F | Exemption of 20% on the standard for repair and expenditure |

| taxable net value (E-F) |

The property tax rate is 15% of the assessed net value. The annual assessed net value refers to the net rental income for the tax year (January 1 to March 31), after deducting charges, unrecoverable rent, and repair costs.

The repair cost varies depending on the property’s condition. To simplify the calculation process, the tax authority automatically deducts 20% of the owner’s net rental income as a standard tax-free allowance for repairs and expenses. This 20% covers all incidental costs arising from the lease, and the owner is not required to provide actual expense documentation to the tax authority.

If a tenant defaults on rent payments, the landlord must calculate the unpaid rent when filing property tax. If the landlord determines the rent cannot be recovered, they may apply for a deduction from the rent income.

Can property maintenance costs be deducted based on actual expenses?

No, the tax authority only accepts a flat 20% deduction of total income (see the example above for details). Even if actual expenses exceed the 20% deduction threshold, the calculation must strictly follow the 20% deduction rule.

Example of property tax calculation

For the 2020/21 tax year, the property’s monthly rent was $20,000, with annual maintenance charges amounting to $8,000. Due to the pandemic, the tenant began defaulting on rent in March 2021. The landlord has been unable to contact the tenant and has not received the March 2021 rent payment to date.

| A | rent income | 240,000.00 |

| B | unrecoverable rent | (20,000.00) |

| C | Appraised Taxable Value (A-B) | 220,000.00 |

| D | rates paid by owners | (8,000.00) |

| E | (C-D) | 212,000.00 |

| F | Exemption of 20% on the standard for repair and expenditure | (42,400.00) |

| taxable net value (E-F) | 169,600.00 |

| Property tax will be levied at 15% in 2020/21 fiscal year. | 25,440 |

| Add: Provisional tax for 2021/22 | 25,440 |

| total tax payable | 50,880 |

Property tax due date

The assessment notice will specify the due date. Unless you have objected to the assessment or applied for a deferral of the tax, and have received a notice from the Inland Revenue Department regarding the amount to be deferred, you must pay the tax listed in the assessment notice by the due date or before it.

Property tax is paid in two installments.

The tax assessment notice will specify two payment dates. Typically, the first payment is due in November of the current year, followed by the second payment in April of the following year. This is because, for the provisional tax payment, you should receive seven months ‘rent (from April to October) by the end of October, and the full year’s rent by the end of March.

Can applying for Personal Income Tax exemption save you from Property Tax?

If you own rental properties as an individual and have unused tax credits, you can apply for personal assessment to combine the property’s assessed value with your personal income for tax savings. Additionally, mortgage interest payments on rental properties are deductible under personal assessment but not under property tax.